In 2025, Singapore’s commercial property market quietly shifted gears. Large headline transactions — from Keppel REIT’s $1.45 billion purchase of MBFC Tower 3 stake to Brookfield’s industrial portfolio deals — signalled more than fleeting activity. They marked a broader strategic recalibration of capital that will shape investments well into 2026 and beyond.

This article goes beyond transaction tallies to explain why investors are returning, where they are putting capital, and what this behaviour means for the next stage of the market cycle.

Funding Costs, Asset Repricing: The Real Catalysts

The most significant driver of renewed activity is not a macro cheerfest — it’s funding dynamics.

After a prolonged period of rate volatility and credit caution, financing conditions in Singapore and the broader Asia-Pacific have become more favourable. Lower borrowing costs, coupled with repackaged debt structures, are prompting sponsors and institutional capital to reassess assets that were previously sidelined. Spreads between buyer bids and seller pricing expectations are narrowing, and that alone is unlocking deals that have been dormant for quarters.

This is critical. Capital isn’t pouring back because sentiment has recovered fully — it’s returning because leverage is once more operationally viable and risk pricing is better discovered.

Office: Quality Wins, But Broad Revival Is Not Here Yet

Despite global narratives of “office dead,” Singapore’s office market tells a more nuanced story. Domestic and cross-border capital remain interested in Grade-A, core Central Business District (CBD) space, where tenant demand and limited new supply underpin resilience. This is evidenced by marquee investments such as CapitaSpring and the South Beach stake sale.

But this doesn’t mean a broad, across-the-board revival. The office sector remains bifurcated:

This divergence is normal in real estate cycles — quality assets trade because they offer visibility and predictability, not speculative upside.

Industrial: The Backbone of Transaction Volume

While office headlines grab attention, industrial real estate accounted for the largest proportion of transaction volume over the first nine months of 2025.

This reflects a simple truth: long-lease, large-corporate tenants with strong credit profiles are inherently attractive during periods of macro uncertainty. Industrial assets — especially logistics, cold storage, data centres and specialised facilities — offer predictable cash flows that are less sensitive to short-term economic shocks. These attributes make them defensive and growth-oriented — a rare duality.

Local market data also show industrial rents and prices holding steady, with prime logistics rents edging upward mid-2025 — a sign that fundamentals remain robust rather than speculative.

Living Sector: Capital Chasing Income Stability

The living sector — particularly serviced residences and rental housing — is gaining traction among institutional investors. Singapore’s high occupancy rates, rental growth since 2019, and structural constraints on new supply make this segment appealing.

Investors view living assets not as a hedge on owner-occupied demand, but as income assets backed by demographic fundamentals — assets that yield relatively stable returns even in uncertain macro conditions.

Importantly, punitive additional buyer’s stamp duty (ABSD) measures have indirectly bolstered rental demand by deterring speculative ownership, shifting capital toward income-producing living assets.

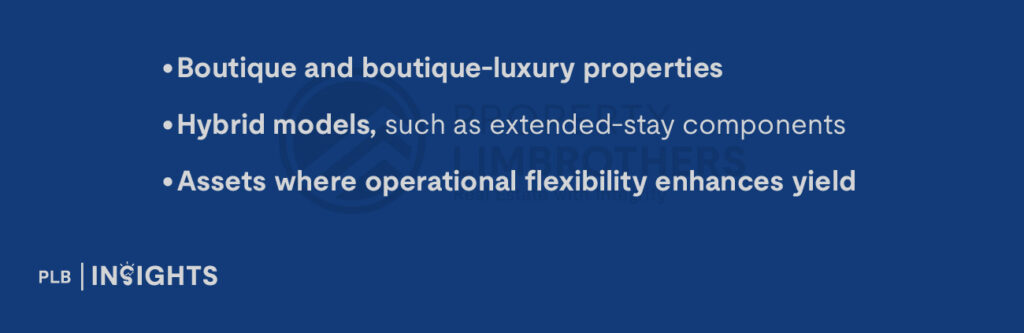

Hotels & Hospitality: Smaller Tickets, Strategic Plays

Contrary to the view that tourism alone fuels hotel demand, the reality in Singapore is more strategic. Investors have shown preference for:

These niche formats attract private equity and yield-seeking capital because they allow active management — a way to generate alpha even if macro conditions remain uncertain.

While tourism recovery remains important, the current draw lies in operational differentiation, not visitor numbers alone.

Portfolio Strategy: Value Add Over Core

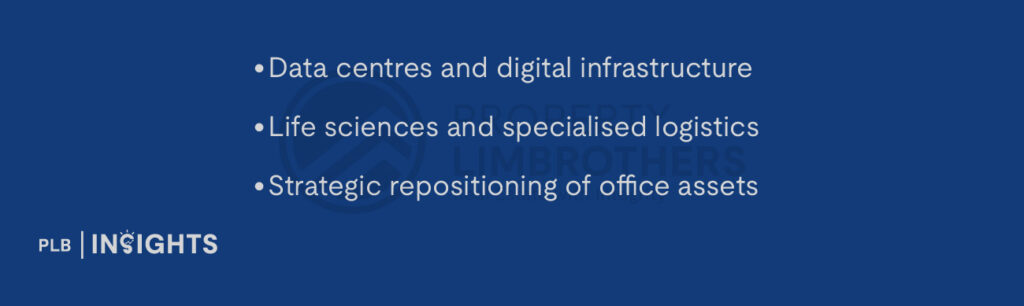

A notable shift in capital strategy is underway. Traditional core investment has ceded ground to value-add plays — where investors believe they can enhance income or reposition assets to generate returns through active management rather than passive ownership.

This trend aligns with global patterns where capital seeks operational uplift rather than pure rental yield compression. Investors are increasingly comfortable allocating to:

Value-add strategies now outnumber core and core-plus strategies among Asia-Pacific real estate funds, highlighting a tactical pivot toward sectors with growth levers beyond cyclical rent gains.

Singapore Capital Going Global: Diversification, Not Retreat

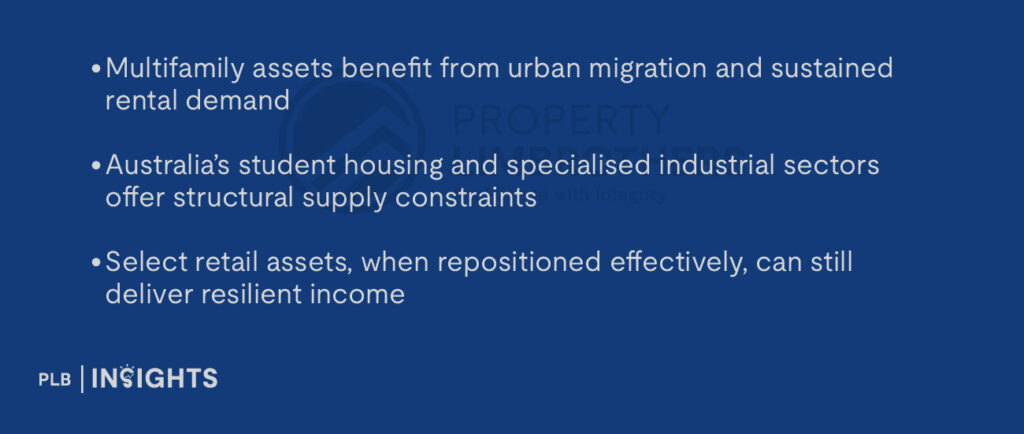

Singapore investors aren’t just buying locally. They are deploying capital overseas in search of resilient income streams, particularly in markets such as Japan and Australia where demographics and long-term fundamentals remain supportive.

This outbound activity isn’t capital flight. It reflects strategic diversification — a hallmark of mature capital allocation:

Such diversification enables portfolio resilience even if certain domestic sectors face near-term headwinds.

Underlying Fundamentals vs Sentiment

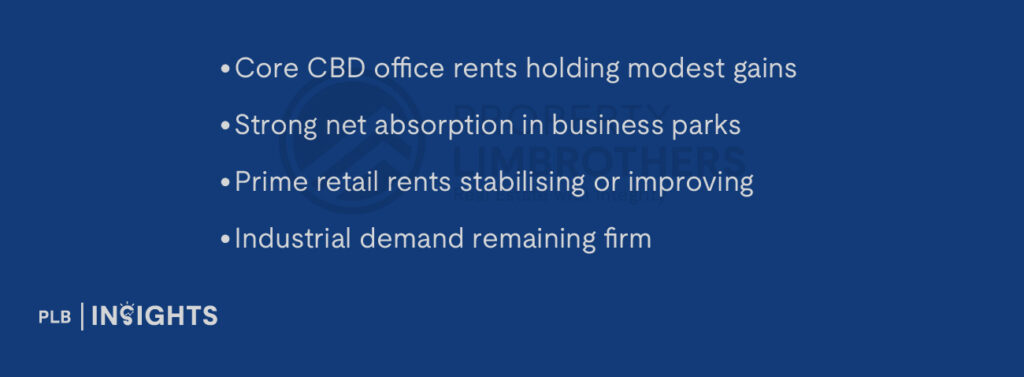

Across sectors, fundamentals paint a steadier picture than market sentiment suggests.

Recent data indicate:

These trends underscore that Singapore’s real estate ecosystem remains anchored by real economic activity, not speculative capital flows.

Looking Ahead: What 2026 May Hold

Rather than attempting precise forecasts, capital behaviour offers clearer signals about the next phase of the cycle.

Selective Activity Will Prevail

Investors are likely to remain focused on high-conviction assets and sectors, rather than broad-based market exposure.

Debt Markets Will Remain Central

Access to competitive financing will continue to determine deal feasibility and transaction velocity.

Operational Capability Will Drive Returns

Active asset management — particularly in logistics, living, and alternative sectors — will matter more than timing alone.

Singapore’s Fundamentals Will Continue to Command a Premium

Regulatory clarity, liquidity, and macro stability remain core strengths that underpin investor confidence.

In essence, 2026 looks set to be a year of disciplined capital deployment rather than exuberant expansion.

Conclusion: Reading Capital, Not Headlines

The story of Singapore’s commercial real estate market in 2025 is not one of exuberant recovery, but of measured re-engagement.

Investors are not chasing momentum. They are responding to:

What we are witnessing is not a speculative upswing, but a strategic repositioning of capital in a market where resilience matters more than speed.

The takeaway is simple: Singapore’s commercial property market is not booming — it is stabilising, maturing, and quietly positioning for durability.

Every cycle creates different entry points across assets and sectors. For a clearer view of how today’s commercial market is evolving, connect with our sales consultants for a focused discussion.