In recent months, the United Kingdom’s housing market has slipped into an unusual kind of stagnation — not a crash, not a soft landing, but a pause. The Royal Institution of Chartered Surveyors (RICS) reported that the index of homes put up for sale fell to –20 in October, the third straight month of decline and the weakest reading since 2021. Buyer enquiries have weakened, sales volumes have thinned and agents across the country now report downward pressure on prices, especially in London and higher-value segments.

The most striking part of this slowdown is not the numbers themselves — it is the timing. The UK market is cooling before any new policies are announced. The Labour government will only present its budget on 26 November, yet the market has already pulled back sharply. Sellers are waiting. Buyers are waiting. Developers are signalling slower sales. Retailers are reporting subdued consumer confidence. The entire ecosystem is in a holding pattern.

This raises a much bigger question:

What happens to housing markets when policy uncertainty — not policy itself — becomes the main driver of sentiment?

And what lessons can Singapore draw from this moment?

This article builds on the themes explored in our earlier article, “Big Countries, Big Land… Big Housing Crisis. Tiny Singapore? Not So.” — where we saw how housing outcomes are shaped not by land size or national wealth but by system design, long-term planning and disciplined governance. The UK’s current pause offers a real-time example of how fragile housing markets can be when predictability breaks down.

The UK’s Sudden Cooldown: A Market Waiting for Clarity

RICS’ October data paints a sobering picture. Listings have fallen rapidly, reflecting a sharp rise in seller hesitation. Buyer demand is dropping in tandem, with agents reporting weaker enquiries and slower deal flow. Prices in the £1 million and above segments — common in London and the South — are now softening more visibly.

What triggered this?

Not a collapse in borrowing affordability, not a surge in supply, and not a macroeconomic shock.

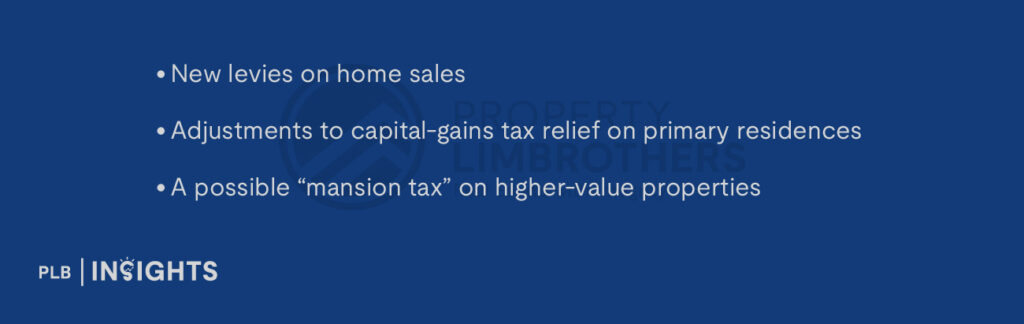

Instead, the fear centres around potential fiscal changes. According to media reports, the Treasury is evaluating:

None of these have been confirmed. Yet the anticipation alone is strong enough to freeze activity.

Buyers fear buying into a shifting tax framework. Sellers worry about being caught by new levies. Developers highlight softer sales pipelines. Retailers see households delaying discretionary purchases like electronics — a sign that caution is broad-based, not just housing-specific.

The message is clear: in today’s environment, uncertainty can slow a housing market faster than interest rates can.

The Mechanics of a Sentiment Freeze

What is happening in the UK is emblematic of how modern housing markets behave under uncertainty:

Buyers avoid locking themselves into an unpredictable future

A home purchase is a long-term decision. If future transaction costs, capital-gains treatment or tax exposures become murky, many simply pause. It is rational behaviour.

Sellers hesitate because the “right time” suddenly disappears

Uncertainty can distort seller expectations. If taxes on sales rise, they would prefer to wait. If prices fall, they might delay listing. In the UK, both fears are circulating simultaneously, creating a standstill.

Developers and builders face planning risk

Forward sales slow, land bids become more cautious, and new projects may be deferred. For a country already struggling with a tight supply pipeline, this puts additional strain on future delivery.

High-end markets feel the chill first

Because they are most sensitive to changes in capital-gains rules and wealth-related taxation, the £1M+ segments freeze faster. Agents are already reporting weaker interest in these tiers.

Sentiment, in other words, has become a central force — capable of halting activity before any real changes take effect.

A Structural Fragility Exposed

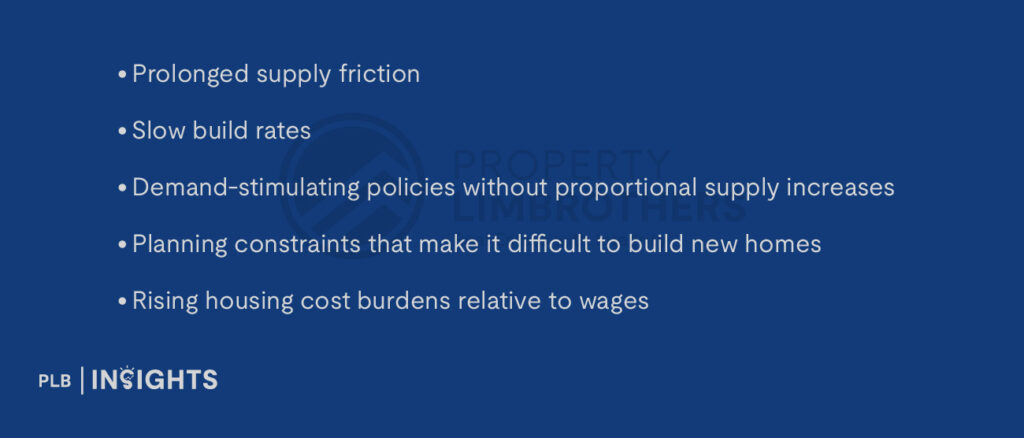

In our earlier article, we reviewed how advanced economies like the UK, Canada and Australia arrived at affordability crises despite large land mass and strong national wealth. The UK, in particular, faced:

These structural weaknesses created a market that was already stretched. The current fiscal uncertainty is not the root cause of the slowdown — it is the catalyst that revealed the underlying fragility.

When base conditions are weak, even a rumour can tilt the balance.

Why This Moment Matters for Singapore Homebuyers

The UK’s experience offers a valuable reminder for homeowners, buyers and policymakers here: in housing markets, predictability is not a luxury — it is a stabiliser.

Singapore is not immune to global trends, nor are our housing prices low. But one structural advantage has consistently underpinned stability:

a predictable, coherent housing framework anchored by long-term planning.

Clear and sequenced policy design

Singapore’s housing policies, whether demand-side rules such as Loan To Value (LTV) and Total Debt Servicing Ratio (TDSR) or supply-side measures such as land release, are typically implemented with clarity and rationale. Buyers and sellers can plan decisions around known frameworks rather than sudden shifts.

A transparent land-release system

Singapore’s Government Land Sales (GLS) programme provides visibility around future supply. This reduces the risk of sellers rushing to beat policy changes or buyers delaying decisions due to unclear pipelines.

Systematic — not reactive — demand management

Cooling measures are used periodically but consistently, with an eye on long-term stability rather than budget balancing.

This matters because sentiment thrives on clarity. Even in years of rising interest rates or inflation, Singapore did not experience the kind of sudden freezes seen in markets where policy uncertainty dominates.

A Global Trend: Fiscal Pressure Means More Policy Risk Everywhere

The UK’s current challenge does not exist in isolation. Around the world, governments face:

When national budgets tighten, property markets often become candidates for taxation or policy adjustment because they represent large pools of private wealth.

This means policy risk — real or perceived — is likely to become more common across developed nations.

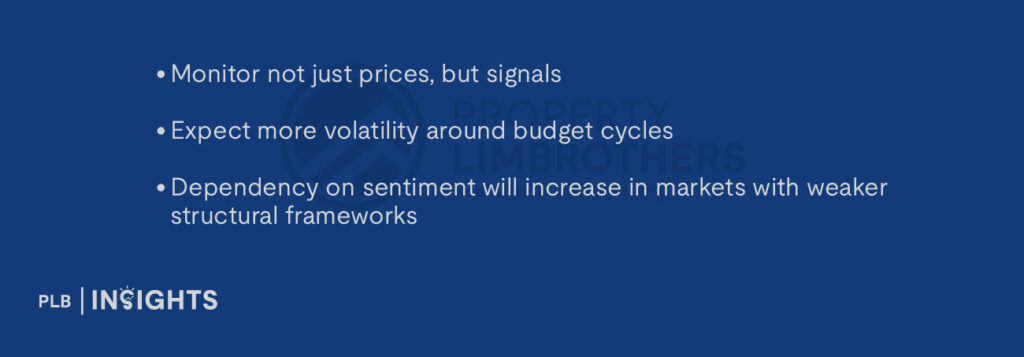

What This Means For Investors and Homeowners

Clarity will become one of the most valuable characteristics of a housing system.

What Singapore Households Should Pay Attention To

While our system is more stable, global trends still matter. For homeowners and buyers, three areas deserve attention:

Economic fundamentals

Household incomes, interest rate trends and job stability continue to shape housing demand more than short-term sentiment.

Supply pipelines

Upcoming BTO launches, GLS sites, and private supply can influence pricing dynamics meaningfully.

Policy signalling

Singapore’s approach emphasises early, clear communication. Even then, keeping an eye on policy direction can help homeowners plan upgrading or right-sizing strategies more confidently.

Conclusion: A Pause Is a Message, Not a Mystery

The UK housing market’s freeze is not a crash — it is a message. It shows that housing markets today are highly sensitive to uncertainty, even before any policy is implemented. Structural weaknesses can lie dormant for years, but clarity — or the lack of it — can swiftly bring them to the surface.

For Singapore, the lesson is not that other countries “struggle” while we do not. Rather, it is that housing stability is engineered through design, not luck. Predictability, long-term planning and transparent communication remain essential in an era where global volatility is the norm.

As markets around the world navigate fiscal pressures, inflation shifts and demographic change, one principle becomes increasingly clear:

In the housing market, confidence is a force as real as supply and demand. And confidence is built on clarity.

If you are planning your next property move, understanding the system behind the market — not just the prices in front of you — will be the key to making informed decisions with long-term confidence.

If you’re planning your next property step, our consultants are ready to help you navigate it with clarity and confidence.